Look at where all the energy is going right now. Private listings. Walled gardens. Google plugging into MLS supply. MLSs suing each other. Every fight in this business is a fight over the same thing, which is who controls the homes for sale.

So Dan Cooper and the Gitcha crew zigged. They built a listing type for the other side of the trade. Not the houses. The buyers.

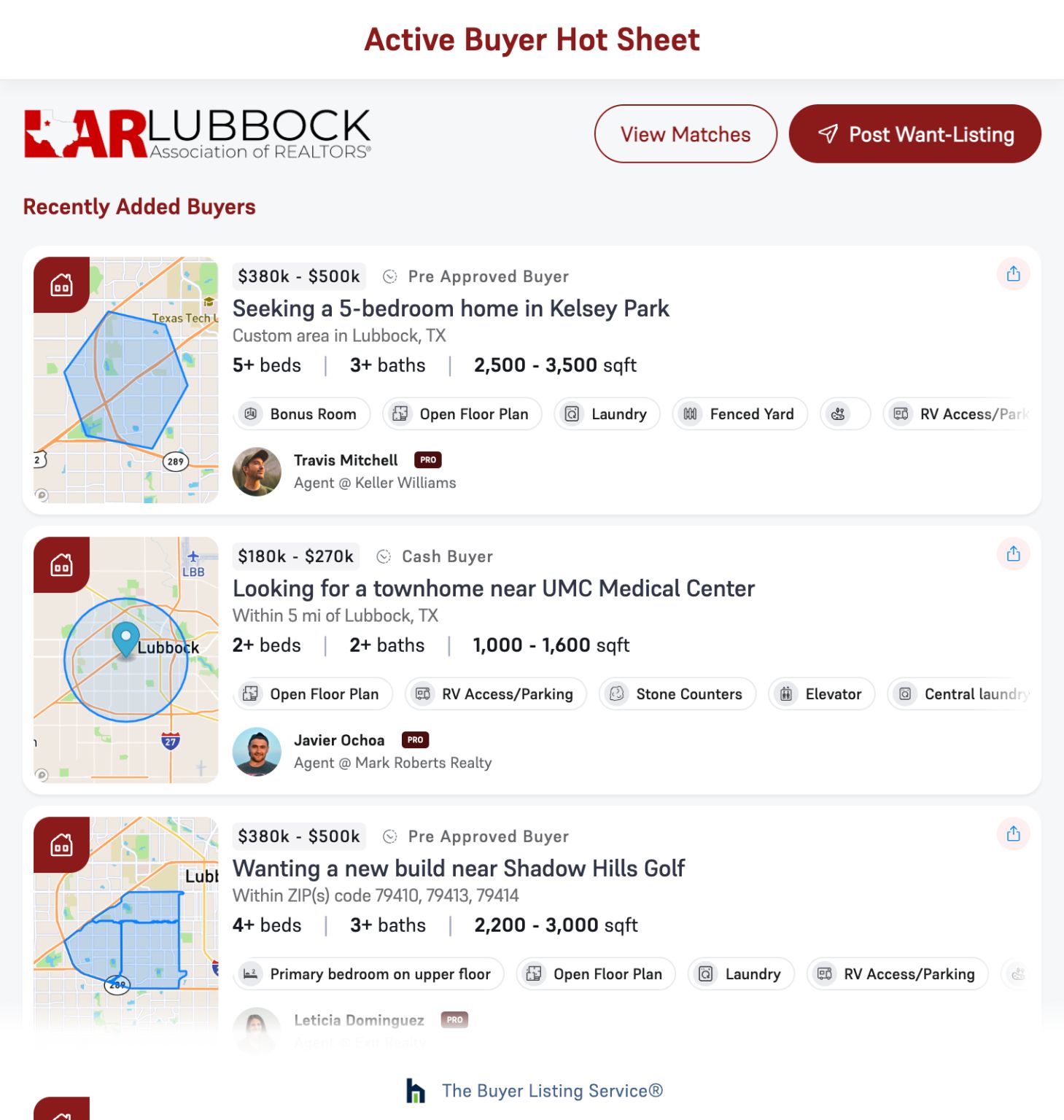

They call it the Buyer Listing Service, and the core unit is a Want-Listing. Location, property type, budget, financing, timeline, buyer agreement status. Structured buyer demand, published into the MLS, visible to the whole network. Here’s their line:

It’s not a search. It’s a listing for buyers.

Dan and his team and Gitcha came back on my radar with a LinkedIn post on their “𝗔𝗰𝘁𝗶𝘃𝗲-𝗕𝘂𝘆𝗲𝗿 𝗛𝗼𝘁 𝗦𝗵𝗲𝗲𝘁 𝗗𝗮𝘀𝗵𝗯𝗼𝗮𝗿𝗱 𝗪𝗶𝗱𝗴𝗲𝘁.”

I’m here for it. While everyone else is busy hiding supply, Gitcha is publishing demand. A buyer listing is the structural twin of a pocket listing, and that’s the smart part. In a world where the supply side goes quiet, the leverage shifts to whoever knows the buyers. They’re building the answer to the problem the rest of the industry is busy creating.

The CMA angle is the one that got me, and this was my turf. Their pitch to listing agents is “walk into the listing appointment with data nobody else has.” Active buyer count, price clustering, demand trends. Their line: “CMA shows what sold. This shows who’s buying right now.” A CMA is a rearview mirror. This is the windshield. If it actually works, that’s a real reason to walk in the door.

It’s early. Three MLSs so far. Lubbock in April, MIBOR later that month, Momentum in western Arizona in June. The tell to watch is the vendor integration. Gitcha claims it’s already working with 4 of the top 5 MLS vendors to embed this natively. If that ships, this gets interesting fast. If it doesn’t, it’s another good idea on three dashboards.

You don’t change this industry from a breakout session. You change it by building the thing nobody asked for yet. And nobody ever wins big betting on the establishment.

{kind=link}